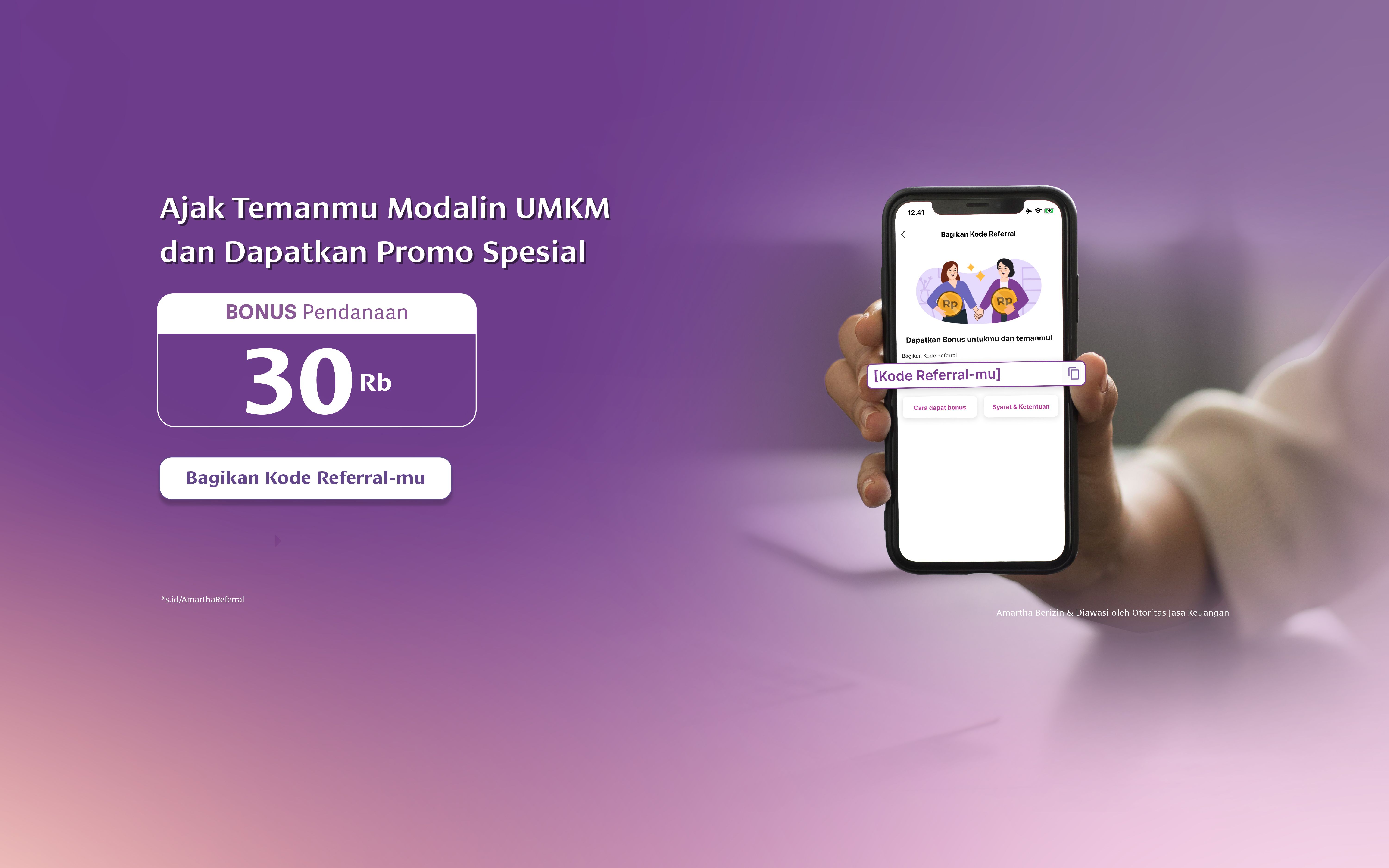

Mempersiapkan keberlanjutan bersama Amartha

Melayani keuangan mikro dan pendanaan berkelanjutan

Memberdayakan UMKM perempuan beserta keluarga dan lingkungannya

Mendorong pertumbuhan yang lebih inklusif dengan memajukan perekonomian pedesaan

Beragam Solusi Amartha untuk Kesejahteraan Merata

Untuk Individu

Pilihan solusi finansial berupa pinjaman dan pendanaan untuk individu hingga pemilik UMKM

Untuk Bisnis

Pilihan solusi pendanaan yang berdampak sosial bagi perusahaan atau instansi

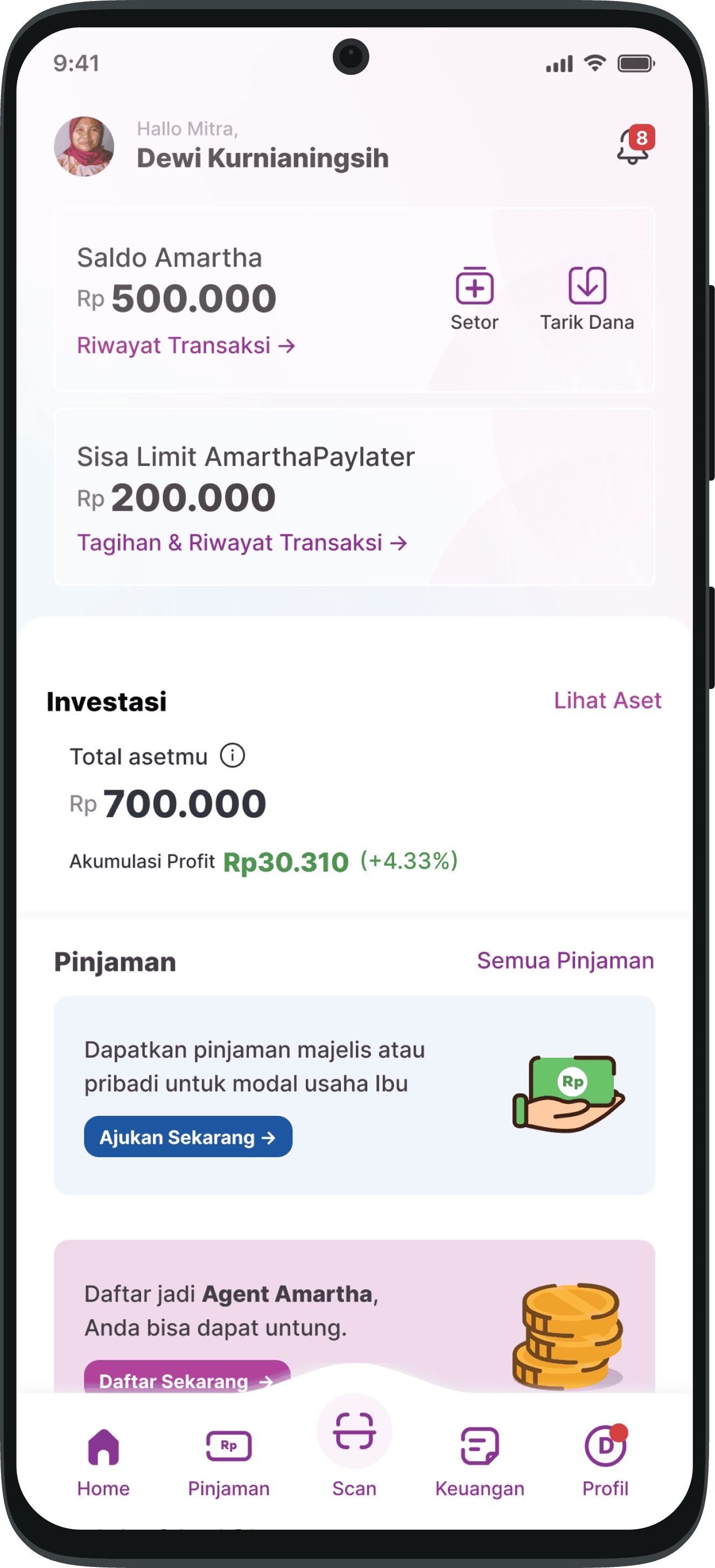

Dukungan Finansial

Kembangkan UMKM dengan pinjaman modal usaha

Pinjaman Kelompok

Ajukan pinjaman modal usaha dalam kelompok 15-20 orang

PELAJARIPaylater

Memudahkan transaksi harian dengan limit hingga Rp500 ribu

PELAJARIPinjaman Modal Kerja

Pinjaman modal tanpa jaminan aset untuk mendukung pengeluaran bisnis

PELAJARIPinjaman Multiguna

Pinjaman individu untuk beragam kebutuhan

PELAJARI

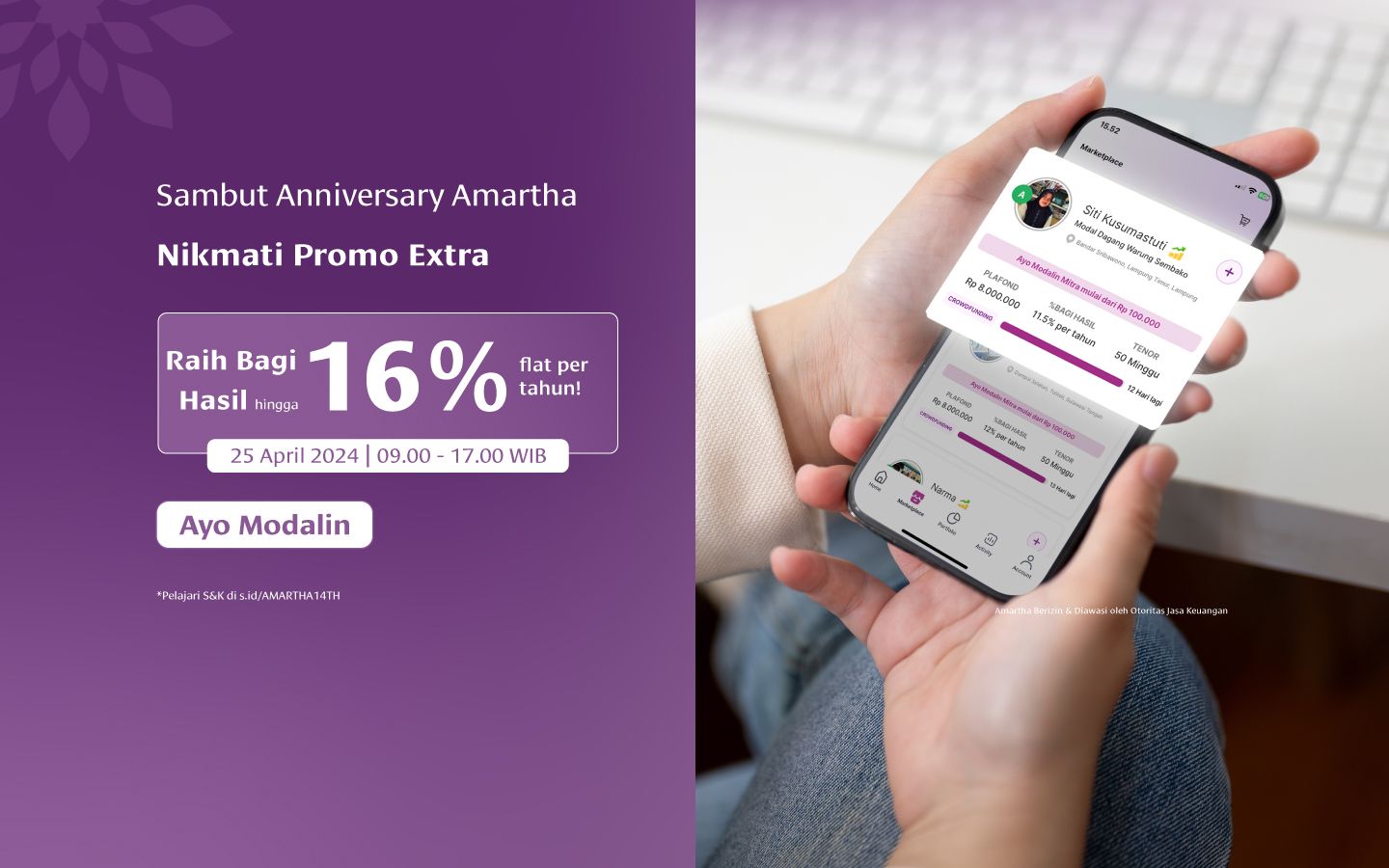

Pendanaan Berdampak

Kembangkan aset finansial dengan keuntungan lebih prediktif untuk wujudkan kesejahteraan yang merata

Solusi andalan dari Amartha

Semua yang Anda butuhkan untuk kembangkan aset

Sertifikasi dan Penghargaan untuk Komitmen dan Kualitas Amartha

News and Promo

Rayakan Anniversary ke-14 Amartha dan Nikmati Berbagai Promonya!

BACA ARTIKEL

Modalin UMKM di Akhir Pekan Dampaknya Berkelanjutan

BACA ARTIKEL

Modalin UMKM Saat Liburan, Dampaknya Terus Berkelanjutan

BACA ARTIKEL

Nikmati Promo Pendanaan di Hari Kemenangan

BACA ARTIKEL

UMKM Go Digital, Apa Tujuannya?

BACA ARTIKEL

Apa Itu Microfinance? Berikut Pengertian, Sejarah, dan Fungsinya

BACA ARTIKEL

Menuju Hari Kemenangan Saatnya Ciptakan Kebaikan lewat Pendanaan

BACA ARTIKEL

Modalin UMKM di Akhir Pekan Dapatkan Bonusnya, Dukung Kesejahteraan

BACA ARTIKEL

Berizin dan Diawasi oleh Otoritas Jasa Keuangan